Rightmove Plc (RMV.L)

Dow Jones, Bloomberg, & Rightmove

Welcome back to The Berkshire Backstop. Today’s post contains some musings on moats and a short analysis of Rightmove Plc. I hope you enjoy.

“Only the Paranoid Survive”

A large dosage of paranoia goes a long way when running a business. Some of the greatest businesses of all time have been killed by underdogs. The rare exceptions that survive competition tend to have some combination of three key qualities:

1. An enduring culture which strives to defend and widen the moat.

2. An asset so irreplaceable that the business can handle some mismanagement.

3. A Chief Executive (usually the founder) who is a generational talent.

These qualities bring several iconic case studies to mind: the success of the Costco system, the power of Coca-Cola’s brand, and the capital allocation brilliance of Henry Singleton at Teledyne. Each business thrived over a long period of time, despite fierce competition, proving that their competitive advantages were truly durable.

Since the invention of the internet, a new class of exceptional businesses emerged and left a trail of casualties in their wake. Take Google, whose irreplaceable search asset helped kill some of the world’s best business models: telephone directories, encyclopaedias, and Newspapers etc. These businesses had dominant market shares controlled by vast network effects. They earned phenomenal returns on capital and grew quickly while gushing out cash. And for a while, it seemed like this could go on forever. The market valued them as if they were government-backed perpetuities.

Most eventually became worthless. The best of them survived, but they exist now as shadows of their former selves. Despite this, many of the long-term owners of these businesses did extremely well from the sheer amount of cash received in dividends.

My question is as follows: was the decline of these once great businesses inevitable or could a stronger gene for paranoia have saved them?

Michael Bloomberg, how to build a wonderful business.

The Dow Jones Industrial Average has been around for 130 years. Created by Charles Dow and Edward Jones in 1896, it opened at 41 — it was back at 41 in 1932 — and today it sits at around 50,000. By the 1950s, the Dow had beaten out other averages and had become the single metric of choice to track the performance of the US stock market.

In addition to the success of the average, which did wonders for the Dow Jones & Company brand, Dow Jones had several valuable assets, two of which were particularly treasured:

1. The Wall Street Journal.

2. The Dow Jones ticker service.

They owned the premier financial newspaper and had the news ticker in nearly every brokerage house in the United States. Combine this with the fact that the second half of the 20th century would see an enormous increase in demand for financial information, it was a truly fantastic hand to be dealt. They had two seemingly irreplaceable assets and were in pole position to lead the world of financial information, and until the 1980s, they did.

In an alternate universe, where John Gutfreund didn’t fire Michael Bloomberg from Salomon Brothers, Dow Jones might have been worth many tens (possibly hundreds) of billions more than the $5bn price Rupert Murdoch’s News Corp paid for it in 2007. But sadly, for the Bancroft family (the owners of Dow Jones) Gutfreund fired Bloomberg and wrote him a $10m check for his stake in the Salomon Brothers partnership.

“When it came to knowing the relative value of one security versus another, most of Wall Street in 1981 had pretty much remained where it was when I began as a clerk in the 1960s: a bunch of guys using no. 2 pencils, chronicling the seat-of-the-pants guesses of too many bored traders.”

- Michael Bloomberg, Bloomberg on Bloomberg

Armed with $10m and an extreme work-ethic, Bloomberg set out to build the tools he’d wished he had when he was at Salomon. Before Bloomberg, each of the largest securities firms collected data independently and relied on hand-held calculators to manipulate information. Bloomberg realised that a firm that could, for example, instantly know whether government bonds were appreciating at a faster rate than corporate bonds would have an enormous competitive advantage over those that couldn’t.

By 1982, Bloomberg (then known as Innovative Market Systems) had its first client. Merrill Lynch purchased the first 22 terminals and liked them so much that they bought 30% of the company for $30m. By the end of the decade Bloomberg terminals were present in every major brokerage, central bank, and even the Vatican.

In 1988, the Wall Street Journal decided to run a front page editorial on Bloomberg. Astonishingly, the Journal was flattering, even printing feedback from a Bloomberg customer who praised the product and disparaged their largest competitor, Telerate: in which Dow Jones had a 60% stake!

Bloomberg continued to outclass Dow Jones, even poaching Matthew Winkler from the Journal to start Bloomberg’s news service, and they had a long runway. The 80s and 90s saw a huge expansion in government debt, the birth of securitisation, a legendary bull market in equities, and the rise of Japan as a financial powerhouse. Each of these tailwinds created an explosion in demand for financial information, and once Bloomberg got their foot in the door, no one was going to replace them.

Bloomberg’s customers are very reluctant to change. Even as Bloomberg’s data advantages were slowly competed away, a better, more durable competitive advantage emerged. Traders spend hours learning how to use it, setting up their exact preferences often containing their own superstitions and rituals. These habits entrench themselves over time and build an extreme reluctance to change, even if it makes financial sense. Suppose you are a trader making over $1m a year, are you seriously going to change provider to save $10k on a cheaper version of Bloomberg? No chance, they have you hooked.

“I’d like to buy into that retroactively”

While the Bancroft family walked away from the Dow Jones & Company billionaires, surely, they must have felt some agony at the opportunity they’d missed. It is easy for us to criticise their lack of imagination as to what could have been done in the financial field, but things must be put into perspective. They owned a hugely profitable organisation which paid out almost all its earnings in dividends and had a moat which seemed impenetrable. Faced with the same hand, I would expect the vast majority of CEOs to have similarly modest results.

Could a better (more paranoid) CEO at Dow Jones have prevented Bloomberg’s rise? This question was once posed to Charlie Munger by Warren Buffett at the 2015 Berkshire AGM:

WARREN BUFFETT: If Tom Murphy had had the hand, it would have been in the hundreds of billions, wouldn’t it?

CHARLIE MUNGER: Well, I don’t know. I’m not sure if we had had that hand we would have…

WARREN BUFFETT: Well, I’m not so sure about us. I’m talking about Murph.

CHARLIE MUNGER: Well, I think even Murph is more like us than he is like Bill Gates. I think it’s hard to invent entirely new modalities and so on.

WARREN BUFFETT: I think Bill Gates would have done well with Dow Jones, too.

CHARLIE MUNGER: Yes. He might.

WARREN BUFFETT: I’d like to buy into that retroactively.

Classified Adverts

Advertising was once a gold mine for the newspaper industry. Newspapers in high circulation or with local strongholds could charge top dollar for access to its thousands of customers. The cheapest ads available were the classified ads, which were usually packed into dense columns. If you wanted to sell your bike, car, or home: these gave you the best bang for your buck.

When the eyeballs drifted away from the newspapers and towards the internet, so too did the classified adverts. Dedicated websites began to appear, aggregating the adverts into specialised categories: properties, autos, recruitment etc. These specialised websites proved to be far more successful for advertisers than traditional newspapers. The people looking for houses went to the websites that advertised houses, it was really that simple. Eventually the mathematical advantage of network effects began to take centre stage for the leading websites: the more eyeballs, the more adverts, and so on.

Soon there were websites that commanded practically complete monopolies, and best of all, they required zero incremental capital to grow: and grow they did, while distributing huge amounts of cash in the process. Investors sat pretty, cashing their dividend cheques and watching share repurchases slowly increase their stakes, as they once did with the beloved Newspaper stocks. We don’t yet know whether this story has a happier ending for the shareholders of classifieds than the shareholders of Newspaper stocks. But a new character has emerged, and the plot is getting interesting.

Artificial Intelligence is quickly becoming the most profound change to the global economy since the internet. Eyeballs are beginning to drift towards AI chat-bots/agents and the potential effect on classifieds is alarming. In Stripe's 2025 annual letter, John Collison outlined what he views as the future of “agentic commerce”, which he defines as: “the idea that your AIs will soon be buying stuff on your behalf.” His vision of agentic commerce has five levels:

Eliminating web forms.

Descriptive search (you stop searching for products and start describing situations).

Persistence (the system already knows your preferences from past interactions).

Delegation (the system makes purchasing decision).

Anticipation (the system anticipates your needs, making purchasing decisions)

Applying Collison’s framework, things begin to look precarious for classifieds. One can quickly envision a world where AI agents scour through estate-agent listings, understanding your exact preferences and sending you notifications for properties that get close to your ideal home (although I’d wager that we’ll never reach levels 4 & 5 for buying real estate).

Rightmove Plc

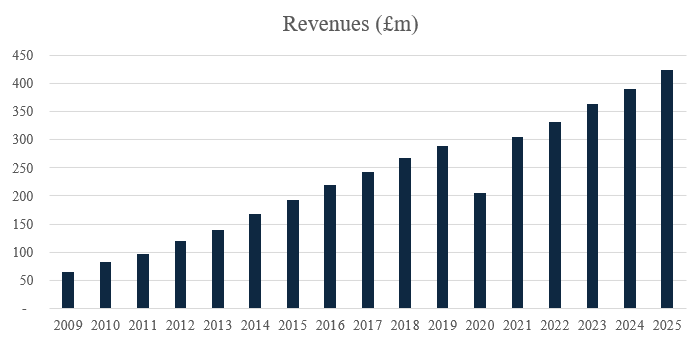

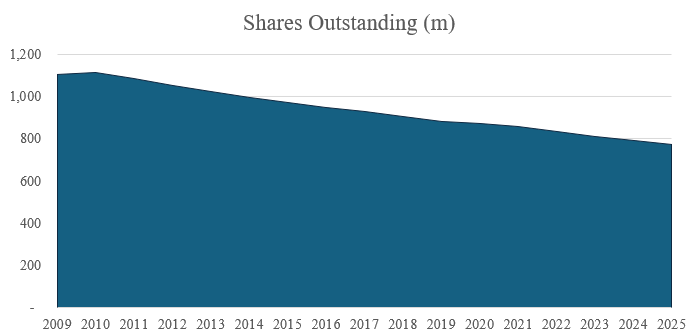

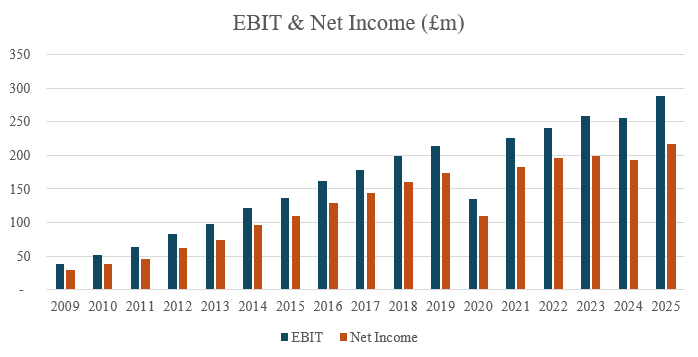

While we’re on the subject of real estate, I’d like to discuss the specific fortunes of the UK’s largest property marketplace. Rightmove was founded in 2000 by four leading corporate estate agencies. At the time, the UK’s property advertising market was fragmented across thousands of regional newspapers and physical shop windows. Rightmove quickly began to gain share, and by 2004 it had 50% of UK estate agents listing properties on the website. Eventually, Rightmove’s lead in customer traffic would become insurmountable: commanding over 80% of the time spent on property portals in the UK.

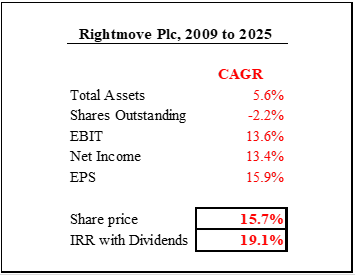

Those kinds of numbers can make any investor dreamy-eyed, but the question at hand is what those numbers will look like over the next 20 years. Until very recently, the stock market thought it knew the answer. It wasn’t uncommon for Rightmove to trade at free cash flow yields between 4% and 3%, reflecting an extremely high degree of conviction that their competitive position wouldn’t change over the next 20 years. That sentiment has changed rapidly.

The latest LLMs are already a very effective way of gathering information, one must assume that in 10 years’ time they will become even more so. Descriptive search and persistence can help to find properties that meet your exact criteria: without the need for endlessly scrolling on property portals. If this happens, Rightmove quickly loses its ability to charge estate agents for prominence in searches. This has been a core part of Rightmove’s ability to increase advertising spend, as there is a proven ROI when estate agents pay extra for ‘featured’ and ‘premium’ listings. Should this happen, Rightmove’s wonderful network effects begin to erode. If eyeballs shift from the portal to AI agents, estate agents may no longer feel compelled to list on Rightmove, since AI systems could surface properties directly from the agents’ own websites. At this point the jig is up, and Rightmove’s toll booth is gone.

How Deep Is your Moat?

High returns on capital don’t make moats; moats make high returns on capital. Investors who claim that the XYZ company has a moat because it earns 50% on capital are committing the same logical fallacy as saying increased umbrella sales lead to bad weather. In fact, a high return on capital isn’t worth much at all if it can’t be maintained over an extended period.

Given Rightmove’s extraordinary returns on capital, numerous well-capitalised competitors have tried to seize their economic castle.

Here are just some of the attackers:

Zoopla. Founded in 2007, Zoopla commands a 10% share of traffic. While they have built a relatively strong position as a distant second, they haven’t been able to usurp Rightmove’s position with consumers and sellers. If you’re selling your house (probably the biggest financial decision of your life) you list on the portal with 80%, not 10%, of the traffic.

OnTheMarket (OTM). Founded in 2015, OTM launched with a restrictive “one other portal” rule: preventing agents from listing on more than one competitor. Most agents who listed on OTM dropped Zoopla instead of Rightmove, causing OTM to eat into Zoopla’s share as opposed to Rightmove’s.

Boomin. Founded in 2021, liquidated in 2022…

Google. In 2009, Google began integrating properties into Google Maps. Google shut down the feature in 2011 due to low usage. Ultimately map based search failed as consumers preferred the portal experience.

Despite competent competition, Rightmove’s competitive position has held firm and continues to get stronger. But while Rightmove’s history of competitiveness is impressive, I could have made a longer list of competition that certain newspapers fought off. For example, The New York Times was founded in 1851 and fought off other papers for over 150 years, but while no newspaper could hurt them, it was the internet that changed the whole ball game.

It’s comforting to take refuge in historical analogy, but every situation is different. AI could be even more profound that the internet, but it might not kill the classified business model. It’s one thing to have an LLM to buy you some new trainers, but buying a house is something entirely different.

Buying & selling a home.

The buying or selling of a home is one of the largest financial transactions of people’s lives: with the average UK house price of £370k and £655k in London. Given the magnitude of the numbers at play and with loss aversion in full force, 90% of sellers still use high-street estate agents who charge a percentage-based commission which is far higher than the flat rates of online brokers. With nearly a quarter of property transactions falling through, sellers are rightly risk averse.

Given the risk averse attitude of sellers, can we expect buyers to suddenly outsource their property search to an AI bot? I’m not so sure. The first problem with an AI search is that most people don’t know exactly what they want until they see it, scrolling on Rightmove helps solve this problem. The second problem is that the value added by an AI search is mostly in its advisory capacity (which areas have the best schools etc), but once a buyer’s requirements are set, a live verified inventory of houses becomes hugely valuable.

For AI agents to usurp Rightmove there is also the problem of changing habits. While the pace of change grows faster over time, old habits still die hard. In 2025, 16.8 billion minutes were spent on Rightmove (up 2.4% from 2024) and ARPA increased by 7.5%. If AI is a threat: it’s not showing up in the numbers just yet.

The counter argument here is that the adoption of LLMs has been faster than any other technology in history (GPT3 had over 100 million users within 2 months of launch) and if AI is widely being implemented into education and the workplace, it shouldn’t take long before AI agents become part of our daily routines. But there are several barriers which slow the pace of change.

The first of which is that finding a house is the least stressful part of the buying process. Mortgage arrangements and conveyancing are pain points which can take up to 20 weeks in total. So, the perceived value of a better search model is somewhat minimal.

The second is the inertia built up by Rightmove’s network effects along with some sticky incentives. Take the following scenario:

Suppose tomorrow morning, you inherit a property and decide to sell it. Like all sellers you will want as much money as possible and fast! So, like the other 90% of sellers, you’re willing to pay an estate agent a commission because your incentives are aligned.

Would you really be happy with that agent not listing your property on the website which sees over 80% of the traffic? Obviously not.

Now suppose the estate agent tells you that their commission will be slightly lower because they won’t have to pay £1530 per month for Rightmove, would your answer change? Of course not, the commission is only 1% of the transaction. What matters is maximising the 99%!

Now suppose they tell you, “Not to worry because the property will still appear on Gemini and ChatGPT, soon everyone will be finding their properties on there.” Are you persuaded yet? Not even slightly. What seller wants to be a guineapig for the mass adoption of property search LLMs at the expense of losing 80% of their potential buyers?

If there is going to be a change in this field, I find it likely that it will happen slowly, and that it can only be driven by buyers. So long as Rightmove maintains the traffic, the moat is intact.

Conclusions, or lack thereof.

This year, Rightmove plans to spend an additional £18m (£12m expensed and £6m capex) on AI related features to improve their offering, this investment phase is due to continue through 2027 and 2028. Perhaps some of this spend is to repay some technical debt, but either way, improving the product offering isn’t a bad idea, particularly with added competition potentially looming.

It’s also important to acknowledge that Rightmove has become a somewhat broader business to what it was 20 years ago. Newer product areas like rental, mortgages, and commercial property continue to grow faster than the core business and have the potential to become very large. I am nervous to call it an ecosystem, but Rightmove’s brand and vast data advantages do leave them in a strong position to grow revenue and earnings at rate similar to (if not faster) than recent historical advantages, if AI doesn’t stop them.

At the moment that is a big if. The current direction seems to be that AI platforms are keen to partner with Rightmove. Rightmove has launched a beta for AI search in partnership with Gemini and a Rightmove app is soon to launch in ChatGPT. This structure makes sense for the AI providers and Rightmove: the AI providers don’t have to do the grunt work of maintain relationships with nearly 20,000 estate agents, and Rightmove don’t have to spend billions of dollars on data centres.

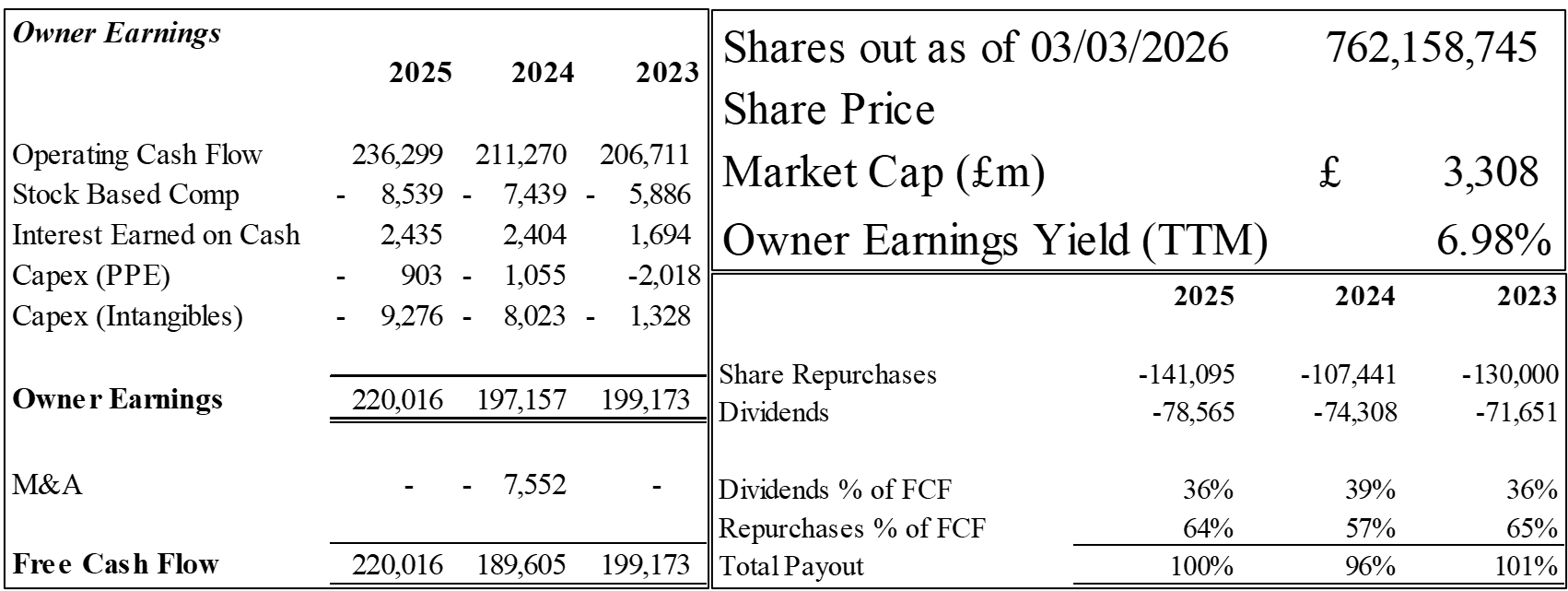

Despite this, I remain apprehensive. The pace of change in tech continues to astonish me, and none of us can be certain what’s going to happen. While a 7% free cash flow yield is attractive in comparison to historic valuations, it still requires a degree of confidence in the next 20 years that I don’t have. My inability to quantify the odds of success or failure puts this investment into the “too hard pile” for now. However, that may well change. At some point valuations can become ridiculously cheap, as they did with some Newspaper stocks after the financial crisis. And I might find a way to improve my confidence in Rightmove’s competitive position. But until then, I’m blissfully undecided.

All the best,

Ben

Disclaimer: Nothing in this post constitutes investment advice, a recommendation to buy or sell any security. The content is for informational and educational purposes only and reflects personal opinions at the time of writing. DO YOUR OWN RESEARCH!

I've been re-reading Berkshire's annual reports in chronological order, and it's so interesting to see Buffett gloat about how great businesses like the Buffalo News and World Book were. On the flip side, looking at Berkshire's performance, it's proof you have ample time to pivot in investing.

Great article, only the paranoid survive. This one’s definitely in the too hard for me pile.